Las condiciones previas para la crisis financiera fueron complejas y multifacéticas. [5] [6] [7] Casi dos décadas antes, el gobierno de los EE. UU. había aprobado una legislación que permitía una financiación más flexible para promover la vivienda asequible. [8] En 1999, se derogaron partes de la legislación Glass-Steagall , lo que permitía a las instituciones financieras mezclar operaciones de bajo riesgo, como la banca comercial y los seguros , con operaciones de mayor riesgo, como el comercio por cuenta propia y la banca de inversión . [9]

Se podría decir que el mayor factor que contribuyó a las condiciones necesarias para el colapso financiero fue el rápido desarrollo de productos financieros dirigidos a compradores de viviendas de bajos ingresos y escasa información, que en su mayoría pertenecían a minorías raciales . [10] Este desarrollo del mercado no fue atendido por los reguladores y, por lo tanto, tomó por sorpresa al gobierno de los EE. UU . [11]

Mapa mundial que muestra las tasas de crecimiento del PIB real en 2009 (los países en marrón estaban en recesión)Participación del sector financiero de Estados Unidos en el PIB desde 1860 [21]

La crisis desencadenó la Gran Recesión , que, en ese momento, fue la recesión mundial más grave desde la Gran Depresión. [22] [23] [24] [25] [26] También fue seguida por la crisis de la deuda europea, que comenzó con un déficit en Grecia a fines de 2009, y la crisis financiera islandesa de 2008-2011 , que involucró la quiebra bancaria de los tres principales bancos de Islandia y, en relación con el tamaño de su economía, fue el mayor colapso económico sufrido por cualquier país en la historia. [27] Fue una de las cinco peores crisis financieras que el mundo había experimentado y condujo a una pérdida de más de $ 2 billones de la economía mundial. [28] [29] La deuda hipotecaria de vivienda de EE. UU. en relación con el PIB aumentó de un promedio de 46% durante la década de 1990 a 73% durante 2008, alcanzando $ 10,5 (~ $ 14,6 billones en 2023) billones. [30] El aumento de las refinanciaciones con retiro de efectivo , a medida que subían los valores de las viviendas, impulsó un aumento del consumo que ya no podía sostenerse cuando los precios de las viviendas bajaron. [31] [32] [33] Muchas instituciones financieras poseían inversiones cuyo valor se basaba en hipotecas de viviendas, como títulos respaldados por hipotecas o derivados de crédito utilizados para asegurarlos contra quiebras, cuyo valor se redujo significativamente. [34] [35] [36] El Fondo Monetario Internacional estimó que los grandes bancos estadounidenses y europeos perdieron más de un billón de dólares en activos tóxicos y préstamos incobrables desde enero de 2007 hasta septiembre de 2009. [37]

La falta de confianza de los inversores en la solvencia bancaria y la disminución de la disponibilidad de crédito llevaron a una caída en picado de los precios de las acciones y las materias primas a finales de 2008 y principios de 2009. [38] La crisis se extendió rápidamente a un shock económico mundial, lo que resultó en varias quiebras bancarias . [39] Las economías de todo el mundo se desaceleraron durante este período debido a que el crédito se endureció y el comercio internacional disminuyó. [40] Los mercados de la vivienda sufrieron y el desempleo se disparó, lo que resultó en desalojos y ejecuciones hipotecarias . Varias empresas fracasaron. [41] [42] Desde su pico en el segundo trimestre de 2007 en $ 61,4 billones, la riqueza de los hogares en los Estados Unidos cayó $ 11 billones, a $ 50,4 billones a finales del primer trimestre de 2009, lo que resultó en una disminución del consumo, luego una disminución de la inversión empresarial. [43] [44] En el cuarto trimestre de 2008, la disminución trimestral del PIB real en los EE. UU. fue del 8,4%. [45] La tasa de desempleo en Estados Unidos alcanzó un máximo del 11,0% en octubre de 2009, la más alta desde 1983 y aproximadamente el doble de la tasa anterior a la crisis. Las horas promedio por semana laboral descendieron a 33, el nivel más bajo desde que el gobierno comenzó a recopilar los datos en 1964. [46] [47]

La crisis económica comenzó en los EE. UU. pero se extendió al resto del mundo. [41] El consumo estadounidense representó más de un tercio del crecimiento del consumo global entre 2000 y 2007 y el resto del mundo dependió del consumidor estadounidense como fuente de demanda. [ cita requerida ] [48] [49] Los valores tóxicos eran propiedad de inversores corporativos e institucionales a nivel mundial. Los derivados como los swaps de incumplimiento crediticio también aumentaron el vínculo entre las grandes instituciones financieras. El desapalancamiento de las instituciones financieras, ya que los activos se vendieron para pagar obligaciones que no podían refinanciarse en mercados crediticios congelados, aceleró aún más la crisis de solvencia y causó una disminución del comercio internacional. Las reducciones en las tasas de crecimiento de los países en desarrollo se debieron a caídas en el comercio, los precios de las materias primas, la inversión y las remesas enviadas por los trabajadores migrantes (ejemplo: Armenia [50] ). Los estados con sistemas políticos frágiles temían que los inversores de los estados occidentales retiraran su dinero debido a la crisis. [51]

Como parte de la respuesta de la política fiscal nacional a la Gran Recesión , los gobiernos y los bancos centrales, incluida la Reserva Federal , el Banco Central Europeo y el Banco de Inglaterra , proporcionaron billones de dólares en rescates y estímulos sin precedentes en ese momento, incluida una política fiscal y monetaria expansiva para compensar la disminución del consumo y la capacidad de préstamo, evitar un mayor colapso, alentar los préstamos, restaurar la confianza en los mercados integrales de papel comercial , evitar el riesgo de una espiral deflacionaria y proporcionar a los bancos fondos suficientes para permitir que los clientes realicen retiros. [52] En efecto, los bancos centrales pasaron de ser el " prestamista de última instancia " al "prestamista de única instancia" para una parte significativa de la economía. En algunos casos, la Fed fue considerada el "comprador de última instancia". [53] [54] [55] [56] [57] Durante el cuarto trimestre de 2008, estos bancos centrales compraron US$2,5 billones (~$3,47 billones en 2023) de deuda gubernamental y activos privados en problemas de los bancos. Esta fue la mayor inyección de liquidez en el mercado crediticio y la mayor medida de política monetaria en la historia mundial. Siguiendo un modelo iniciado por el paquete de rescate bancario del Reino Unido de 2008 , [58] [59] los gobiernos de las naciones europeas y los Estados Unidos garantizaron la deuda emitida por sus bancos y aumentaron el capital de sus sistemas bancarios nacionales, comprando finalmente 1,5 billones de dólares en acciones preferentes recién emitidas en los principales bancos. [44] La Reserva Federal creó entonces cantidades significativas de nueva moneda como método para combatir la trampa de liquidez . [60]

Los rescates se dieron en forma de billones de dólares en préstamos, compras de activos, garantías y gastos directos. [61] Los rescates estuvieron acompañados de una gran controversia, como en el caso de la controversia sobre los pagos de bonificaciones de AIG , lo que llevó al desarrollo de una variedad de "marcos de toma de decisiones" para ayudar a equilibrar los intereses políticos en competencia durante tiempos de crisis financiera. [62] Alistair Darling , el Ministro de Hacienda del Reino Unido en el momento de la crisis, declaró en 2018 que Gran Bretaña estuvo a horas de "un colapso de la ley y el orden" el día en que se rescató al Royal Bank of Scotland . [63] En lugar de financiar más préstamos internos, algunos bancos gastaron parte del dinero del estímulo en áreas más rentables, como invertir en mercados emergentes y monedas extranjeras. [64]

En total, 47 banqueros cumplieron condena como resultado de la crisis, más de la mitad de los cuales eran de Islandia , donde la crisis fue la más severa y condujo al colapso de los tres principales bancos islandeses. [68] En abril de 2012, Geir Haarde de Islandia se convirtió en el único político en ser condenado como resultado de la crisis. [69] [70] Solo un banquero en los Estados Unidos cumplió condena como resultado de la crisis, Kareem Serageldin , un banquero de Credit Suisse que fue sentenciado a 30 meses de cárcel y devolvió $ 24,6 millones en compensación por manipular los precios de los bonos para ocultar $ 1 mil millones de pérdidas. [71] [68] Ningún individuo en el Reino Unido fue condenado como resultado de la crisis. [72] [73] Goldman Sachs pagó $ 550 millones para resolver los cargos de fraude después de supuestamente anticipar la crisis y vender inversiones tóxicas a sus clientes. [74]

Al haber menos recursos para arriesgar en la destrucción creativa, el número de solicitudes de patentes se mantuvo estable, en comparación con los aumentos exponenciales de las solicitudes de patentes en años anteriores. [75]

Porcentaje de ingresos que va al 1% más rico de los que más ganan, una medida de la desigualdad económica en Estados Unidos entre 1913 y 2008.

Las familias típicas estadounidenses no tuvieron buena suerte, ni tampoco las familias "ricas pero no más ricas" que se encuentran justo debajo de la cima de la pirámide. [76] [77] [78] Sin embargo, la mitad de las familias más pobres de los Estados Unidos no sufrieron ninguna disminución de su riqueza durante la crisis porque, en general, no poseían inversiones financieras cuyo valor puede fluctuar. La Reserva Federal encuestó a 4.000 hogares entre 2007 y 2009 y descubrió que la riqueza total del 63% de todos los estadounidenses disminuyó en ese período y que el 77% de las familias más ricas tuvieron una disminución de su riqueza total, mientras que sólo el 50% de las que se encuentran en la base de la pirámide sufrieron una disminución. [79] [80] [81]

Cronología

A continuación se presenta una cronología de los principales acontecimientos de la crisis financiera, incluidas las respuestas gubernamentales y la posterior recuperación económica. [82] [83] [84] [85]

Antes de 2007

Costo de la vivienda por Estado del año 2000 al 2022

19 de mayo de 2005: el gestor de fondos Michael Burry cerró un CDS contra bonos hipotecarios de alto riesgo con el Deutsche Bank por un valor de 60 millones de dólares, el primero de ese tipo. Proyectó que se volverían volátiles en un plazo de dos años a partir del vencimiento de la baja "tasa de interés inicial" de las hipotecas. [86] [87]

2006: Después de años de aumentos de precios superiores a la media, los precios de la vivienda alcanzaron su punto máximo y la morosidad de los préstamos hipotecarios aumentó, lo que llevó a la burbuja inmobiliaria de los Estados Unidos . [88] [89] Debido a los estándares de suscripción cada vez más laxos, un tercio de todas las hipotecas en 2006 fueron préstamos de alto riesgo o sin documentación, [90] que comprendieron el 17 por ciento de las compras de viviendas ese año. [91]

Mayo de 2006: JPMorgan advierte a sus clientes sobre la crisis del mercado inmobiliario, especialmente el de alto riesgo. [92]

Agosto de 2006: La curva de rendimiento se invirtió, lo que indicaba que probablemente se produciría una recesión dentro de uno o dos años. [93]

Noviembre de 2006: UBS hizo sonar "la alarma sobre una crisis inminente en el mercado inmobiliario de Estados Unidos" [92]

2007 (enero-agosto)

27 de febrero de 2007: Los precios de las acciones en China y los EE. UU. cayeron a su nivel más alto desde 2003, ya que los informes sobre una disminución en los precios de las viviendas y los pedidos de bienes duraderos avivaron los temores sobre el crecimiento, y Alan Greenspan predijo una recesión. [94] Debido al aumento de las tasas de morosidad en los préstamos de alto riesgo , Freddie Mac dijo que dejaría de invertir en ciertos préstamos de alto riesgo. [95]

30 de julio de 2007: IKB Deutsche Industriebank , la primera víctima bancaria de la crisis, anuncia su rescate por parte de la institución financiera pública alemana KfW . [102]

31 de julio de 2007: Bear Stearns liquidó los dos fondos de cobertura. [98]

9 de agosto de 2007: BNP Paribas bloqueó los retiros de tres de sus fondos de cobertura con un total de 2.200 millones de dólares en activos bajo gestión , debido a "una evaporación completa de la liquidez", lo que hizo imposible la valoración de los fondos, una clara señal de que los bancos se negaban a hacer negocios entre ellos. [99] [103] [104]

16 de agosto de 2007: El índice Dow Jones de Irlanda del Norte (DJIA) cierra en 12.945,78 tras caer 12 de los 20 días de negociación anteriores a su pico. Había caído 1.164,63 puntos o un 8,3%. [101]

2007 (septiembre-diciembre)

Personas haciendo cola fuera de una sucursal de Northern Rock en el Reino Unido para retirar sus ahorros durante la crisis financiera

26 de noviembre de 2007: Los mercados estadounidenses entran en una corrección a medida que las preocupaciones sobre el sector financiero siguen aumentando. [112]

12 de diciembre de 2007: La Reserva Federal instituyó la facilidad de subasta a plazo para suministrar crédito a corto plazo a los bancos con hipotecas de alto riesgo. [114]

19 de diciembre de 2007: la agencia de calificación Standard and Poor's rebaja las calificaciones de muchas aseguradoras monolineales que pagan bonos que fracasan. [ cita requerida ]

31 de diciembre de 2007: A pesar de la volatilidad durante la última parte del año, los mercados cierran por encima de donde comenzaron el año, y el DJIA cerró en 13.264,82, un 6,4% más en el año. [116]

18 de enero de 2008: Los mercados bursátiles cayeron a un mínimo anual debido a la rebaja de la calificación crediticia de Ambac , una compañía de seguros de bonos . Mientras tanto, un aumento en la cantidad de retiros hace que Scottish Equitable implemente demoras de hasta 12 meses para las personas que desean retirar dinero. [118]

22 de enero de 2008: La Reserva Federal de Estados Unidos redujo las tasas de interés en un 0,75% para estimular la economía, la mayor caída en 25 años y el primer recorte de emergencia desde 2001. [119]

Enero de 2008: Las acciones estadounidenses tuvieron el peor enero desde el año 2000 debido a las preocupaciones sobre la exposición de las empresas que emiten seguros de bonos . [120]

17 de marzo de 2008: Bear Stearns , con 46.000 millones de dólares en activos hipotecarios que no se habían amortizado y 10 billones de dólares en activos totales, se enfrentaba a la quiebra; en su lugar, en su primera reunión de emergencia en 30 años, la Reserva Federal acordó garantizar sus préstamos incobrables para facilitar su adquisición por parte de JPMorgan Chase por 2 dólares por acción. Una semana antes, la acción cotizaba a 60 dólares por acción y un año antes cotizaba a 178 dólares por acción. El precio de compra se incrementó a 10 dólares por acción la semana siguiente. [124] [125] [126]

18 de marzo de 2008: En una reunión polémica, la Reserva Federal redujo la tasa de fondos federales en 75 puntos básicos, su sexto recorte en seis meses. [127] También permitió a Fannie Mae y Freddie Mac comprar 200.000 millones de dólares en hipotecas de alto riesgo a los bancos. Los funcionarios pensaron que esto contendría la posible crisis. El dólar estadounidense se debilitó y los precios de las materias primas se dispararon. [ datos faltantes ] [128] [129] [130]

Finales de junio de 2008: A pesar de que el mercado de valores de Estados Unidos cayó un 20% desde sus máximos, las acciones relacionadas con las materias primas se dispararon, ya que el petróleo se cotizó por encima de los 140 dólares por barril por primera vez y los precios del acero superaron los 1.000 dólares por tonelada. Las preocupaciones por la inflación combinadas con la fuerte demanda de China alentaron a la gente a invertir en materias primas durante el auge de las materias primas de la década de 2000. [ 131] [132]

11 de julio de 2008: IndyMac fracasó. Los precios del petróleo alcanzaron un máximo de 147,50 dólares [133] [119]

15 de septiembre de 2008: Después de que la Reserva Federal se negara a garantizar sus préstamos como lo hizo con Bear Stearns, la quiebra de Lehman Brothers provocó una caída de 504,48 puntos (4,42%) en el índice Dow Jones de Londres, su peor caída en siete años. Para evitar la quiebra, Merrill Lynch fue adquirida por Bank of America por 50.000 millones de dólares en una transacción facilitada por el gobierno. [136] Lehman había estado en conversaciones para ser vendido a Bank of America o Barclays, pero ninguno de los bancos quería adquirir la empresa entera. [137]

17 de septiembre de 2008: Los inversores retiraron 144.000 millones de dólares de los fondos del mercado monetario de Estados Unidos , el equivalente a una retirada masiva de fondos de este mercado , que con frecuencia invierten en papel comercial emitido por corporaciones para financiar sus operaciones y nóminas, lo que provocó la congelación del mercado de préstamos a corto plazo. La retirada se compara con los 7.100 millones de dólares retirados la semana anterior. Esto interrumpió la capacidad de las corporaciones para renovar su deuda a corto plazo . El gobierno de Estados Unidos extendió un seguro para las cuentas del mercado monetario análogo al seguro de depósitos bancarios a través de una garantía temporal [139] y con programas de la Reserva Federal para comprar papel comercial.

20 de septiembre de 2008: Paulson solicitó al Congreso de los Estados Unidos que autorizara un fondo de 700 mil millones de dólares para adquirir hipotecas tóxicas, diciéndole al Congreso: "Si no se aprueba, que Dios nos ayude a todos". [141]

29 de septiembre de 2008: Por una votación de 225 a 208, con la mayoría de los demócratas a favor y los republicanos en contra, la Cámara de Representantes rechazó la Ley de Estabilización Económica de Emergencia de 2008 , que incluía el Programa de Alivio de Activos en Problemas de 700 mil millones de dólares . En respuesta, el DJIA cayó 777,68 puntos, o 6,98%, entonces la mayor caída de puntos en la historia. El índice S&P 500 cayó un 8,8% y el Nasdaq Composite cayó un 9,1%. [149] Varios índices bursátiles en todo el mundo cayeron un 10%. Los precios del oro se dispararon a 900 dólares la onza. La Reserva Federal duplicó sus swaps de crédito con bancos centrales extranjeros, ya que todos necesitaban proporcionar liquidez. Wachovia llegó a un acuerdo para venderse a Citigroup; sin embargo, el acuerdo habría hecho que las acciones perdieran su valor y habría requerido financiación gubernamental. [150]

30 de septiembre de 2008: El presidente George W. Bush se dirigió al país y dijo: "El Congreso debe actuar... Nuestra economía depende de una acción decisiva del gobierno. Cuanto antes abordemos el problema, antes podremos volver a la senda del crecimiento y la creación de empleo". El Dow Jones rebotó un 4,7%. [151]

2 de octubre de 2008: Los índices bursátiles cayeron un 4% debido al nerviosismo de los inversores ante la votación en la Cámara de Representantes de Estados Unidos sobre la Ley de Estabilización Económica de Emergencia de 2008. [ 153]

3 de octubre de 2008: La Cámara de Representantes aprobó la Ley de Estabilización Económica de Emergencia de 2008 y el Programa de Alivio de Activos en Problemas de 700 mil millones de dólares. [154] Bush firmó la legislación ese mismo día. [155] Wachovia llegó a un acuerdo para ser adquirida por Wells Fargo en un acuerdo que no requirió financiación gubernamental. [156]

6 al 10 de octubre de 2008: Del 6 al 10 de octubre de 2008, el Dow Jones Industrial Average (DJIA) cerró a la baja en las cinco sesiones. Los niveles de volumen batieron récords. El Dow Jones Industrial Average cayó 1.874,19 puntos, o 18,2%, en su peor caída semanal de la historia tanto en puntos como en porcentaje. El S&P 500 cayó más de 20%. [157]

7 de octubre de 2008: En los EE. UU., en virtud de la Ley de Estabilización Económica de Emergencia de 2008, la Corporación Federal de Seguro de Depósitos aumentó la cobertura del seguro de depósitos a 250.000 dólares por depositante. [158]

Durante la crisis financiera mundial de 2008, el índice SENSEX de la Bolsa de Valores de Boston (BSE) sufrió una fuerte caída: pasó de más de 21.000 puntos en enero de 2008 a menos de 8.000 puntos en octubre de 2008. [159]

8 de octubre de 2008: El mercado de valores de Indonesia suspendió sus operaciones tras una caída del 10% en un día. [160] Los bancos centrales mundiales celebraron reuniones de emergencia y coordinaron recortes de las tasas de interés antes de la apertura de los mercados de valores de Estados Unidos. [161]

11 de octubre de 2008: El director del Fondo Monetario Internacional (FMI) advirtió que el sistema financiero mundial estaba al borde de un colapso sistémico. [162]

14 de octubre de 2008: Después de haber sido suspendido durante tres días hábiles sucesivos (9, 10 y 13 de octubre), el mercado de valores islandés reabrió el 14 de octubre, con el índice principal, el OMX Iceland 15 , cerrando en 678,4, que era aproximadamente un 77% más bajo que los 3.004,6 al cierre del 8 de octubre, después de que el valor de los tres grandes bancos, que habían formado el 73,2% del valor del OMX Iceland 15, se hubiera fijado en cero, lo que llevó a la crisis financiera islandesa de 2008-2011 . [163] La Corporación Federal de Seguro de Depósitos creó el Programa de Garantía Temporal de Liquidez para garantizar la deuda sénior de todas las instituciones aseguradas por la FDIC hasta el 30 de junio de 2009. [164]

16 de octubre de 2008: Se dio a conocer un plan de rescate para los bancos suizos UBS AG y Credit Suisse . [165]

24 de octubre de 2008: Muchas de las bolsas de valores del mundo experimentaron las peores caídas de su historia, con caídas de alrededor del 10% en la mayoría de los índices. [166] En los EE. UU., el DJIA cayó un 3,6%, aunque no tanto como otros mercados. [167] El dólar estadounidense , el yen japonés y el franco suizo se dispararon frente a otras monedas importantes, en particular la libra esterlina y el dólar canadiense , ya que los inversores mundiales buscaron refugios seguros. Se desarrolló una crisis monetaria , con los inversores transfiriendo vastos recursos de capital a monedas más fuertes, lo que llevó a muchos gobiernos de economías emergentes a buscar ayuda del Fondo Monetario Internacional . [168] [169] Más tarde ese día, el vicegobernador del Banco de Inglaterra , Charlie Bean , sugirió que "Esta es una crisis única en la vida, y posiblemente la mayor crisis financiera de su tipo en la historia de la humanidad". [170] En una transacción impulsada por los reguladores, PNC Financial Services acordó adquirir National City Corp. [171]

2008 (noviembre-diciembre)

Restaurante en Bristol , Reino Unido , que anuncia un almuerzo barato para personas con crisis crediticia

6 de noviembre de 2008: El FMI predijo una recesión mundial de -0,3% para 2009. El mismo día, el Banco de Inglaterra y el Banco Central Europeo , respectivamente, redujeron sus tasas de interés del 4,5% al 3%, y del 3,75% al 3,25%. [172]

20 de noviembre de 2008: Islandia obtuvo un préstamo de emergencia del Fondo Monetario Internacional después de que la quiebra de los bancos en Islandia provocara una devaluación de la corona islandesa y amenazara al gobierno con la quiebra. [174]

29 de noviembre de 2008: El economista Dean Baker observó:

Hay una razón muy buena para que el crédito sea más estricto. Decenas de millones de propietarios de viviendas que hace dos años tenían un patrimonio sustancial en sus casas hoy tienen poco o nada. Las empresas se enfrentan a la peor recesión desde la Gran Depresión . Esto es importante para las decisiones crediticias. Es muy poco probable que un propietario con patrimonio en su casa deje de pagar un préstamo para un automóvil o una deuda de tarjeta de crédito. Recurrirá a ese patrimonio en lugar de perder su automóvil y/o que se le incluya una mora en su historial crediticio. Por otra parte, un propietario que no tenga patrimonio es un riesgo grave de impago. En el caso de las empresas, su solvencia depende de sus beneficios futuros. Las perspectivas de beneficios parecen mucho peores en noviembre de 2008 que en noviembre de 2007... Aunque muchos bancos están obviamente al borde del abismo, los consumidores y las empresas tendrían muchas más dificultades para obtener crédito en este momento incluso si el sistema financiero fuera sólido como una roca. El problema de la economía es la pérdida de cerca de 6 billones de dólares en riqueza inmobiliaria y una cantidad aún mayor de riqueza bursátil. [176]

1 de diciembre de 2008: La NBER anunció que Estados Unidos se encontraba en recesión y que así había sido desde diciembre de 2007. El Dow cayó 679,95 puntos o 7,8% tras la noticia. [177] [101]

6 de enero de 2009: Citi afirmó que Singapur experimentaría "la recesión más severa en la historia de Singapur" en 2009. Al final, la economía creció en 2009 un 0,1% y en 2010 un 14,5%. [180] [181] [182]

13 de febrero de 2009: El Congreso aprobó la Ley de Recuperación y Reinversión Estadounidense de 2009 , un paquete de estímulo económico de 787 mil millones de dólares. El presidente Barack Obama lo firmó el 17 de febrero. [184] [13] [185] [186]

20 de febrero de 2009: El DJIA cerró en un mínimo de seis años en medio de preocupaciones de que los bancos más grandes de los Estados Unidos tendrían que ser nacionalizados . [187]

27 de febrero de 2009: El DJIA cerró en su valor más bajo desde 1997, ya que el gobierno de Estados Unidos aumentó su participación en Citigroup al 36%, lo que generó más temores de nacionalización y un informe mostró que el PIB se contrajo al ritmo más rápido en 26 años. [188]

A principios de marzo de 2009: La caída de los precios de las acciones se comparó con la de la Gran Depresión . [189] [190]

3 de marzo de 2009: El presidente Obama declaró que "Comprar acciones es un negocio potencialmente bueno si se tiene una perspectiva a largo plazo". [191]

6 de marzo de 2009: El Dow Jones alcanzó su nivel más bajo de 6.469,95, una caída del 54% desde su pico de 14.164 el 9 de octubre de 2007, en un lapso de 17 meses, antes de comenzar a recuperarse. [192]

10 de marzo de 2009: Las acciones de Citigroup subieron un 38% después de que el director ejecutivo dijera que la empresa había obtenido beneficios en los dos primeros meses del año y expresara optimismo sobre su situación de capital en el futuro. Los principales índices bursátiles subieron entre un 5 y un 7%, lo que marcó el punto más bajo de la caída del mercado bursátil. [193]

12 de marzo de 2009: Los índices bursátiles de Estados Unidos subieron otro 4% después de que el Bank of America dijera que había obtenido beneficios en enero y febrero y que probablemente no necesitaría más financiación gubernamental. Bernie Madoff fue condenado. [194]

Primer trimestre de 2009: Durante el primer trimestre de 2009, la tasa anualizada de disminución del PIB fue del 14,4% en Alemania, 15,2% en Japón, 7,4% en el Reino Unido, 18% en Letonia, [195] 9,8% en la zona del euro y 21,5% en México. [41]

10 de abril de 2009: La revista Time declaró: "Más rápidamente de lo que comenzó, la crisis bancaria ha terminado". [196]

29 de abril de 2009: La Reserva Federal proyectó un crecimiento del PIB de 2,5-3% en 2010; una meseta de desempleo en 2009 y 2010 de alrededor del 10% con moderación en 2011; y tasas de inflación de alrededor del 1-2%. [197]

... el ritmo de la contracción económica se está desacelerando. Las condiciones en los mercados financieros han mejorado en general en los últimos meses. El gasto de los hogares ha mostrado más signos de estabilización, pero sigue limitado por las continuas pérdidas de empleo, la menor riqueza inmobiliaria y la restricción del crédito. Las empresas están reduciendo la inversión fija y la dotación de personal, pero parecen estar logrando avances en la alineación de las existencias con las ventas. Aunque es probable que la actividad económica siga siendo débil durante un tiempo, el Comité sigue anticipando que las medidas de política para estabilizar los mercados e instituciones financieras, el estímulo fiscal y monetario y las fuerzas del mercado contribuirán a una reanudación gradual del crecimiento económico sostenible en un contexto de estabilidad de precios. [199]

27 de enero de 2010: El presidente Obama declaró que "los mercados ahora están estabilizados y hemos recuperado la mayor parte del dinero que gastamos en los bancos". [206]

Primer trimestre de 2010: Las tasas de morosidad en Estados Unidos alcanzaron un máximo del 11,54%. [207]

12 de septiembre de 2010: Los reguladores europeos introdujeron las regulaciones de Basilea III para los bancos, que aumentaron los coeficientes de capital, limitaron el apalancamiento, restringieron la definición de capital para excluir la deuda subordinada, limitaron el riesgo de contraparte y agregaron requisitos de liquidez. [212] [213] Los críticos argumentaron que Basilea III no abordó el problema de las ponderaciones de riesgo defectuosas. Los principales bancos sufrieron pérdidas por la calificación AAA creada por la ingeniería financiera (que crea activos aparentemente libres de riesgo a partir de garantías de alto riesgo) que requerían menos capital según Basilea II. Los préstamos a los soberanos con calificación AA tienen una ponderación de riesgo de cero, lo que aumenta los préstamos a los gobiernos y conduce a la próxima crisis. [214] Johan Norberg argumentó que las regulaciones (Basilea III entre otras) de hecho han llevado a préstamos excesivos a gobiernos riesgosos (ver Crisis de deuda soberana europea ) y el Banco Central Europeo busca aún más préstamos como solución. [215]

Marzo de 2011: Dos años después del punto más bajo de la crisis, muchos índices bursátiles estaban un 75% por encima de sus mínimos establecidos en marzo de 2009. Sin embargo, la falta de cambios fundamentales en los mercados bancarios y financieros preocupó a muchos participantes del mercado, incluido el Fondo Monetario Internacional . [217]

2011: La riqueza familiar media cayó un 35% en Estados Unidos, de 106.591 dólares a 68.839 dólares entre 2005 y 2011. [218]

Agosto de 2012: En Estados Unidos, muchos propietarios de viviendas seguían enfrentándose a ejecuciones hipotecarias y no podían refinanciarlas ni modificarlas. Las tasas de ejecuciones hipotecarias seguían siendo altas. [220]

2014: Un informe mostró que la distribución de los ingresos de los hogares en los Estados Unidos se volvió más desigual durante la recuperación económica posterior a 2008 , una novedad para los Estados Unidos pero en línea con la tendencia de las últimas diez recuperaciones económicas desde 1949. [222] [223] La desigualdad de ingresos en los Estados Unidos creció entre 2005 y 2012 en más de 2 de cada 3 áreas metropolitanas. [224]

Junio de 2015: Un estudio encargado por la ACLU concluyó que los hogares blancos propietarios de viviendas se recuperaron de la crisis financiera más rápido que los hogares negros propietarios de viviendas, lo que amplió la brecha de riqueza racial en los EE. UU. [225]

2017: Según el Fondo Monetario Internacional , de 2007 a 2017, las economías "avanzadas" representaron solo el 26,5% del crecimiento del PIB mundial ( PPA ), mientras que las economías emergentes y en desarrollo representaron el 73,5% del crecimiento del PIB mundial (PPA). [226]

Agosto de 2023: UBS llega a un acuerdo con el Departamento de Justicia de los Estados Unidos para pagar un total de 1.435 millones de dólares en sanciones civiles para resolver un asunto heredado de 2006-2007 relacionado con la emisión, suscripción y venta de valores respaldados por hipotecas residenciales. [227]

En la tabla, los nombres de las economías emergentes y en desarrollo se muestran en negrita, mientras que los nombres de las economías desarrolladas aparecen en tipo romano (regular).

La acción de la Reserva Federal ante la crisis

Proyecto de ley de reforma de la financiación de la vivienda

La expansión de los préstamos del banco central en respuesta a la crisis no se limitó sólo a la prestación de ayuda por parte de la Reserva Federal a las instituciones financieras individuales. La Reserva Federal también ha llevado a cabo una serie de programas de préstamos innovadores con el objetivo de mejorar la liquidez y fortalecer diferentes instituciones financieras y mercados, como Freddie Mac y Fannie Mae . En este caso, el principal problema en el mercado es la falta de reservas de efectivo libres y flujos para garantizar los préstamos. La Reserva Federal tomó una serie de medidas para hacer frente a las preocupaciones sobre la liquidez en los mercados financieros. Una de estas medidas fue una línea de crédito para los principales operadores, que actúan como socios de la Reserva Federal en las actividades de mercado abierto. [229] Además, se establecieron programas de préstamos para flexibilizar los fondos mutuos del mercado monetario y el mercado de papel comercial. Además, se puso en marcha el Term Asset-Backed Securities Loan Facility (TALF) gracias a un esfuerzo conjunto con el Departamento del Tesoro de los EE. UU. Este plan tenía por objeto facilitar a los consumidores y las empresas la obtención de crédito al dar más crédito a los estadounidenses que poseían valores respaldados por activos de alta calidad.

Antes de la crisis, las existencias de títulos del Tesoro de la Reserva Federal se vendieron para pagar el aumento del crédito. Este método tenía por objeto evitar que los bancos trataran de entregar sus ahorros adicionales, lo que podría hacer que la tasa de los fondos federales cayera por debajo del nivel en que se suponía que debía estar. [230] Sin embargo, en octubre de 2008, se le otorgó a la Reserva Federal la facultad de proporcionar a los bancos pagos de intereses sobre sus reservas excedentes. Esto creó una motivación para que los bancos mantuvieran sus reservas en lugar de desembolsarlas, reduciendo así la necesidad de que la Reserva Federal cubriera su mayor concesión de préstamos con reducciones en los activos alternativos. [231]

Los fondos del mercado monetario también sufrieron corridas cuando la gente perdió la fe en el mercado. Para evitar que la situación fuera a peor, la Reserva Federal dijo que daría dinero a las compañías de fondos mutuos. Además, el Departamento del Tesoro dijo que cubriría brevemente los activos del fondo. Ambas cosas ayudaron a que el mercado de fondos volviera a la normalidad, lo que ayudó al mercado de papel comercial, que la mayoría de las empresas utilizan para funcionar. La FDIC también hizo una serie de cosas, como aumentar el límite del seguro de $100,000 a $250,000, para impulsar la confianza de los clientes.

Sistema de la Reserva Federal

Se pusieron en marcha medidas de flexibilización cuantitativa , que sumaron más de 4 billones de dólares al sistema financiero y consiguieron que los bancos volvieran a prestarse dinero, tanto entre ellos como a la gente. Muchos propietarios de viviendas que estaban tratando de evitar que sus casas cayeran en mora consiguieron créditos para la vivienda. Se aprobó un paquete de políticas que permitían a los prestatarios refinanciar sus préstamos aunque el valor de sus viviendas fuera inferior a lo que aún debían por sus hipotecas . [232]

En su informe de enero de 2011, la Comisión de Investigación de la Crisis Financiera (FCIC, un comité de congresistas estadounidenses) concluyó que la crisis financiera era evitable y fue causada por: [234] [235] [236] [237] [238]

"una combinación de endeudamiento excesivo, inversiones riesgosas y falta de transparencia" por parte de las instituciones financieras y de los hogares, que ponen al sistema financiero en una trayectoria de colisión con la crisis.

la mala preparación y la acción inconsistente del gobierno y de los principales responsables de las políticas, que carecían de una comprensión plena del sistema financiero que supervisaban, "lo que aumentó la incertidumbre y el pánico".

un "colapso sistémico de la rendición de cuentas y la ética" en todos los niveles.

"el colapso de las normas de concesión de préstamos hipotecarios y el proceso de titulización de hipotecas".

"los fallos de las agencias de calificación crediticia" a la hora de fijar correctamente el precio del riesgo.

" Wall Street y la crisis financiera: anatomía de un colapso financiero " (conocido como el Informe Levin-Coburn) del Senado de los Estados Unidos concluyó que la crisis fue el resultado de "productos financieros complejos y de alto riesgo; conflictos de interés no revelados; el fracaso de los reguladores, las agencias de calificación crediticia y el mercado mismo para controlar los excesos de Wall Street". [239]

Las altas tasas de morosidad y de impago de los propietarios de viviendas, en particular de aquellos con créditos de alto riesgo, llevaron a una rápida devaluación de los títulos respaldados por hipotecas, incluidas las carteras de préstamos agrupados, los derivados y los swaps de incumplimiento crediticio. A medida que el valor de estos activos se desplomaba, los compradores de estos títulos se evaporaron y los bancos que habían invertido fuertemente en ellos comenzaron a experimentar una crisis de liquidez.

La titulización , un proceso en el que muchas hipotecas se agruparon y se transformaron en nuevos instrumentos financieros llamados títulos respaldados por hipotecas , permitió la transferencia de riesgos y la aplicación de normas de suscripción laxas. Estos paquetes podían venderse como títulos de bajo riesgo (aparentemente), en parte porque a menudo estaban respaldados por un seguro de swap de incumplimiento crediticio . [240] Como los prestamistas hipotecarios podían trasladar estas hipotecas (y los riesgos asociados) de esta manera, podían adoptar, y de hecho lo hicieron, criterios de suscripción laxos.

La regulación laxa permitió préstamos predatorios en el sector privado, [241] [242] especialmente después de que el gobierno federal anulara las leyes estatales anti-predadoras en 2004. [243]

La Ley de Reinversión en la Comunidad (CRA, por sus siglas en inglés), [244] una ley federal estadounidense de 1977 diseñada para ayudar a los estadounidenses de ingresos bajos y moderados a obtener préstamos hipotecarios, exigía a los bancos que otorgaran hipotecas a familias de mayor riesgo. [245] [246] [247] [248] Es cierto que en 2009 los economistas de la Reserva Federal descubrieron que "solo una pequeña parte de las hipotecas de alto riesgo originadas por la CRA" y que "los préstamos relacionados con la CRA parecen tener un rendimiento comparable al de otros tipos de préstamos de alto riesgo". Estos hallazgos "contradicen la afirmación de que la CRA contribuyó de alguna manera sustancial a la [crisis hipotecaria]". [249]

Los préstamos imprudentes por parte de prestamistas como la unidad Countrywide Financial del Bank of America fueron cada vez más incentivados e incluso exigidos por la regulación gubernamental. [250] [251] [252] Esto puede haber causado que Fannie Mae y Freddie Mac perdieran participación de mercado y respondieran bajando sus propios estándares. [253]

Garantías hipotecarias de Fannie Mae y Freddie Mac, agencias cuasi gubernamentales, que compraron muchas titulizaciones de préstamos de alto riesgo. [254] La garantía implícita del gobierno federal de los EE.UU. creó un riesgo moral y contribuyó a un exceso de préstamos riesgosos.

Políticas gubernamentales que incentivaron la adquisición de viviendas, brindando un acceso más fácil a préstamos para prestatarios de alto riesgo; sobrevaluación de hipotecas de alto riesgo agrupadas basadas en la teoría de que los precios de las viviendas seguirían aumentando; prácticas comerciales cuestionables por parte de compradores y vendedores; estructuras de compensación por parte de bancos y originadores de hipotecas que priorizan el flujo de transacciones a corto plazo sobre la creación de valor a largo plazo; y una falta de tenencias de capital adecuadas de los bancos y compañías de seguros para respaldar los compromisos financieros que estaban asumiendo. [255] [256]

La Ley Gramm-Leach-Bliley de 1999 , que derogó parcialmente la Ley Glass-Steagall , eliminó efectivamente la separación entre los bancos de inversión y los bancos depositarios en los Estados Unidos y aumentó la especulación por parte de los bancos depositarios. [257]

La contabilidad a valor razonable fue emitida como la norma de contabilidad estadounidense SFAS 157 en 2006 por el Consejo de Normas de Contabilidad Financiera (FASB), una entidad privada a la que la SEC delegó la tarea de establecer normas de información financiera. [262] Esta exige que los activos comercializables, como los títulos hipotecarios, se valoren de acuerdo con su valor de mercado actual en lugar de su costo histórico o algún valor futuro esperado. Cuando el mercado de dichos títulos se volvió volátil y colapsó, la pérdida de valor resultante tuvo un efecto financiero importante sobre las instituciones que los poseían, incluso si no tenían planes inmediatos de venderlos. [263]

La fácil disponibilidad de crédito en los Estados Unidos, impulsada por grandes entradas de fondos extranjeros después de la crisis financiera rusa de 1998 y la crisis financiera asiática de 1997 (período 1997-1998), condujo a un auge de la construcción de viviendas y facilitó el gasto de consumo financiado con deuda. A medida que los bancos comenzaron a otorgar más préstamos a potenciales propietarios de viviendas, los precios de las viviendas comenzaron a subir. Las normas de concesión de préstamos laxas y el aumento de los precios inmobiliarios también contribuyeron a la burbuja inmobiliaria. Los préstamos de diversos tipos (por ejemplo, hipotecarios, de tarjetas de crédito y para automóviles) eran fáciles de obtener y los consumidores asumieron una carga de deuda sin precedentes. [264] [233] [265]

La caída de los precios también dio lugar a que las viviendas valieran menos que los préstamos hipotecarios, lo que proporcionó a los prestatarios un incentivo financiero para recurrir a la ejecución hipotecaria. Los niveles de ejecuciones hipotecarias se mantuvieron elevados hasta principios de 2014. [267] Drenaron una importante riqueza de los consumidores, perdiendo hasta 4,2 billones de dólares. [268] Los impagos y las pérdidas en otros tipos de préstamos también aumentaron significativamente a medida que la crisis se expandió del mercado inmobiliario a otras partes de la economía. Las pérdidas totales se estimaron en billones de dólares estadounidenses a nivel mundial. [266]

Financiarización : el mayor uso del apalancamiento en el sistema financiero.

Las instituciones financieras, como los bancos de inversión y los fondos de cobertura, así como algunos bancos regulados de manera diferente, asumieron importantes cargas de deuda al proporcionar los préstamos descritos anteriormente y no tenían un colchón financiero suficiente para absorber grandes impagos o pérdidas de préstamos. [269] Estas pérdidas afectaron la capacidad de las instituciones financieras para prestar, lo que desaceleró la actividad económica.

Algunos críticos sostienen que las órdenes gubernamentales obligaron a los bancos a conceder préstamos a prestatarios que antes se consideraban no solventes, lo que dio lugar a normas de suscripción cada vez más laxas y a tasas elevadas de aprobación de hipotecas. [270] [250] [271] [251] Esto, a su vez, condujo a un aumento del número de compradores de viviendas, lo que hizo subir los precios de la vivienda. Esta apreciación del valor llevó a muchos propietarios a pedir préstamos con el valor líquido de sus viviendas como si fuera una ganancia inesperada, lo que dio lugar a un apalancamiento excesivo.

Préstamos de alto riesgo

Los préstamos de alto riesgo en Estados Unidos se expandieron drásticamente entre 2004 y 2006

La flexibilización de las normas de concesión de créditos por parte de los bancos de inversión y los bancos comerciales permitió un aumento significativo de los préstamos de alto riesgo . Los préstamos de alto riesgo no se habían vuelto menos riesgosos; Wall Street simplemente aceptó este mayor riesgo. [272]

Debido a la competencia entre los prestamistas hipotecarios por los ingresos y la cuota de mercado, y cuando la oferta de prestatarios solventes era limitada, los prestamistas hipotecarios relajaron las normas de suscripción y otorgaron hipotecas más riesgosas a prestatarios menos solventes. En opinión de algunos analistas, las relativamente conservadoras empresas patrocinadas por el gobierno (GSE) vigilaban a los originadores de hipotecas y mantenían normas de suscripción relativamente altas antes de 2003. Sin embargo, a medida que el poder de mercado pasó de los titulizadores a los originadores, y a medida que la intensa competencia de los titulizadores privados socavó el poder de las GSE, las normas hipotecarias disminuyeron y proliferaron los préstamos riesgosos. Los préstamos más riesgosos se originaron en 2004-2007, los años de la competencia más intensa entre los titulizadores y la cuota de mercado más baja para las GSE. Las GSE finalmente relajaron sus normas para tratar de alcanzar a los bancos privados. [273] [274]

Una opinión contraria es que Fannie Mae y Freddie Mac lideraron el camino hacia estándares de suscripción relajados, a partir de 1995, al promover el uso de sistemas automatizados de suscripción y evaluación fáciles de calificar, al diseñar productos sin pago inicial emitidos por prestamistas, al promover miles de pequeños corredores hipotecarios y por su estrecha relación con agregadores de préstamos de alto riesgo como Countrywide . [275] [276]

Dependiendo de cómo se definan las hipotecas "de alto riesgo", se mantuvieron por debajo del 10% de todas las hipotecas originadas hasta 2004, cuando aumentaron a casi el 20% y se mantuvieron allí hasta el pico de 2005-2006 de la burbuja inmobiliaria de los Estados Unidos . [277]

El papel de los programas de vivienda asequible

El informe mayoritario de la Comisión de Investigación de la Crisis Financiera , escrito por los seis designados demócratas, el informe minoritario, escrito por tres de los cuatro designados republicanos, los estudios de los economistas de la Reserva Federal y el trabajo de varios académicos independientes, en general, sostienen que la política gubernamental de vivienda asequible no fue la causa principal de la crisis financiera. Aunque admiten que las políticas gubernamentales tuvieron algún papel en causar la crisis, sostienen que los préstamos de las GSE tuvieron un mejor desempeño que los préstamos titulizados por bancos de inversión privados y que algunos préstamos originados por instituciones que tenían préstamos en sus propias carteras.

En su opinión discrepante con el informe mayoritario de la Comisión de Investigación de la Crisis Financiera, el miembro conservador del American Enterprise Institute Peter J. Wallison [278] manifestó que cree que las raíces de la crisis financiera se pueden rastrear directa y principalmente a las políticas de vivienda asequible iniciadas por el Departamento de Vivienda y Desarrollo Urbano de los Estados Unidos (HUD) en los años 1990 y a las compras masivas de préstamos riesgosos por parte de las entidades patrocinadas por el gobierno Fannie Mae y Freddie Mac. Basándose en la información contenida en el caso de fraude de valores de la SEC de diciembre de 2011 contra seis ex ejecutivos de Fannie y Freddie, Peter Wallison y Edward Pinto estimaron que, en 2008, Fannie y Freddie tenían 13 millones de préstamos de baja calidad por un total de más de 2 billones de dólares. [279]

A principios y mediados de la década de 2000, la administración Bush pidió en numerosas ocasiones que se investigaran las cuestiones de seguridad y solidez de las GSE y su creciente cartera de hipotecas de alto riesgo. El 10 de septiembre de 2003, el Comité de Servicios Financieros de la Cámara de Representantes de los Estados Unidos celebró una audiencia, a instancias de la administración, para evaluar las cuestiones de seguridad y solidez y revisar un informe reciente de la Oficina de Supervisión de Empresas de Vivienda Federal (OFHEO) que había descubierto discrepancias contables dentro de las dos entidades. [280] [281] Las audiencias nunca dieron lugar a una nueva legislación o una investigación formal de Fannie Mae y Freddie Mac, ya que muchos de los miembros del comité se negaron a aceptar el informe y, en cambio, reprendieron a la OFHEO por su intento de regulación. [282] Algunos, como Wallison, creen que esto fue una advertencia temprana sobre el riesgo sistémico que el creciente mercado de hipotecas de alto riesgo planteaba al sistema financiero estadounidense, que no fue atendido. [283]

Un estudio del Departamento del Tesoro de los Estados Unidos sobre las tendencias crediticias en 305 ciudades entre 1993 y 1998, realizado en 2000, mostró que 467.000 millones de dólares en préstamos hipotecarios fueron otorgados por prestamistas cubiertos por la Ley de Reinversión en la Comunidad (CRA) a prestatarios y vecindarios de ingresos bajos y medios (LMI), lo que representa el 10% de todos los préstamos hipotecarios de los Estados Unidos durante el período. La mayoría de estos préstamos eran de primera clase. Los préstamos de alto riesgo otorgados por instituciones cubiertas por la CRA constituyeron una participación de mercado del 3% de los préstamos de bajo nivel en 1998, [284] pero en el período previo a la crisis, el 25% de todos los préstamos de alto riesgo se produjeron en instituciones cubiertas por la CRA y otro 25% de los préstamos de alto riesgo tenían alguna conexión con la CRA. [285] Sin embargo, la mayoría de los préstamos de alto riesgo no se hicieron a los prestatarios de LMI a los que apuntaba la CRA, [ cita requerida ] [286] [287] especialmente en los años 2005-2006 que llevaron a la crisis, [ cita requerida ] [288] [287] [289] tampoco encontró ninguna evidencia de que los préstamos bajo las reglas de la CRA aumentaran las tasas de morosidad o que la CRA influyera indirectamente en los prestamistas hipotecarios independientes para que aumentaran los préstamos de alto riesgo. [290] [ verificación necesaria ]

Para otros analistas, el retraso entre los cambios de las normas de la CRA en 1995 y la explosión de los préstamos de alto riesgo no es sorprendente y no exculpa a la CRA. Sostienen que hubo dos causas relacionadas con la crisis: la relajación de las normas de suscripción en 1995 y las tasas de interés ultrabajas iniciadas por la Reserva Federal después del ataque terrorista del 11 de septiembre de 2001. Ambas causas tenían que estar presentes antes de que pudiera producirse la crisis. [291] Los críticos también señalan que los compromisos de préstamos de la CRA anunciados públicamente fueron enormes, totalizando 4,5 billones de dólares en los años entre 1994 y 2007. [292] También argumentan que la clasificación de la Reserva Federal de los préstamos de la CRA como "de primera" se basa en la suposición errónea y egoísta de que los préstamos con tasas de interés altas (3 puntos porcentuales por encima del promedio) son iguales a los préstamos "de alto riesgo". [293]

Otros han señalado que no se concedieron suficientes préstamos de este tipo para provocar una crisis de esta magnitud. En un artículo de la revista Portfolio , Michael Lewis habló con un operador que señaló que "no había suficientes estadounidenses con [mal] crédito que solicitaran [préstamos malos] para satisfacer el apetito de los inversores por el producto final". En esencia, los bancos de inversión y los fondos de cobertura utilizaron la innovación financiera para permitir que se hicieran grandes apuestas, mucho más allá del valor real de los préstamos hipotecarios subyacentes, utilizando derivados llamados swaps de incumplimiento crediticio, obligaciones de deuda colateralizadas y CDO sintéticos .

En marzo de 2011, la FDIC había pagado 9.000 millones de dólares (unos 12.000 millones de dólares en 2023 [294] ) para cubrir las pérdidas por préstamos incobrables en 165 instituciones financieras en quiebra. [295] [296] La Oficina de Presupuesto del Congreso estimó, en junio de 2011, que el rescate a Fannie Mae y Freddie Mac supera los 300.000 millones de dólares (unos 401.000 millones de dólares en 2023 [294] ) (calculado añadiendo los déficits de valor razonable de las entidades a los fondos de rescate directo en ese momento). [297]

En enero de 2010, el economista Paul Krugman sostuvo que el crecimiento simultáneo de las burbujas de precios de los bienes raíces residenciales y comerciales y la naturaleza global de la crisis socavan los argumentos de quienes sostienen que Fannie Mae, Freddie Mac, CRA o los préstamos predatorios fueron las causas principales de la crisis. En otras palabras, se desarrollaron burbujas en ambos mercados a pesar de que sólo el mercado residencial se vio afectado por esas posibles causas. [298]

En contra de Krugman, Wallison escribió: "No es cierto que cada burbuja, incluso una gran burbuja, tenga el potencial de causar una crisis financiera cuando se desinfla". Wallison señala que otros países desarrollados tuvieron "grandes burbujas durante el período 1997-2007", pero "las pérdidas asociadas con las moras e impagos hipotecarios cuando estas burbujas se desinflaron fueron mucho menores que las pérdidas sufridas en Estados Unidos cuando se desinfló la [burbuja] de 1997-2007". Según Wallison, la razón por la que la burbuja inmobiliaria estadounidense (a diferencia de otros tipos de burbujas) llevó a la crisis financiera fue que estuvo respaldada por una enorme cantidad de préstamos de baja calidad, generalmente con pagos iniciales bajos o nulos. [299]

La afirmación de Krugman (que el crecimiento de una burbuja inmobiliaria comercial indica que la política de vivienda estadounidense no fue la causa de la crisis) se ve cuestionada por un análisis adicional. Después de investigar el impago de los préstamos comerciales durante la crisis financiera, Xudong An y Anthony B. Sanders informaron (en diciembre de 2010): "Encontramos evidencia limitada de que el deterioro sustancial en la suscripción de préstamos CMBS [títulos respaldados por hipotecas comerciales] ocurrió antes de la crisis". [300] Otros analistas apoyan la afirmación de que la crisis en el sector inmobiliario comercial y los préstamos relacionados se produjo después de la crisis en el sector inmobiliario residencial. La periodista de negocios Kimberly Amadeo informó: "Los primeros signos de declive en el sector inmobiliario residencial se produjeron en 2006. Tres años después, el sector inmobiliario comercial comenzó a sentir los efectos". [ Verificación necesaria ] [301] Denice A. Gierach, abogada inmobiliaria y contadora pública, escribió:

... la mayoría de los préstamos inmobiliarios comerciales eran buenos préstamos destruidos por una economía realmente mala. En otras palabras, los prestatarios no causaron que los préstamos salieran mal, sino la economía. [302]

Crecimiento de la burbuja inmobiliaria

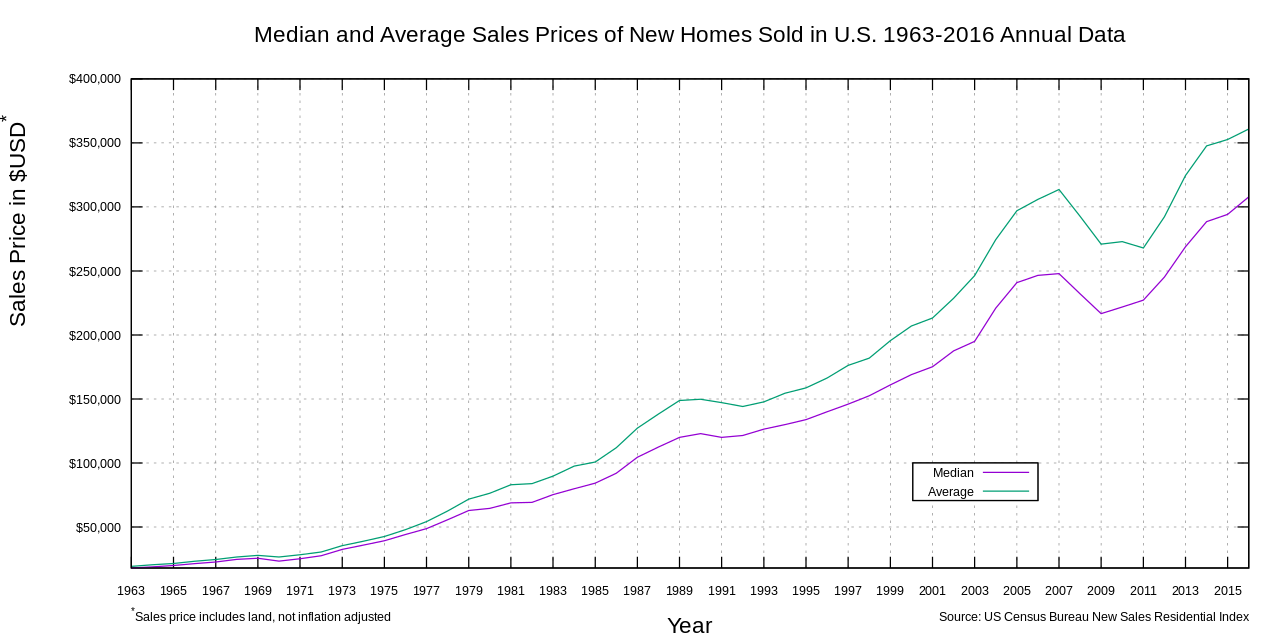

Un gráfico que muestra los precios de venta medianos y promedio de las casas nuevas vendidas en los Estados Unidos entre 1963 y 2016 (sin ajustar por inflación) [88]

Entre 1998 y 2006, el precio de la vivienda típica estadounidense aumentó un 124%. [303] Durante los años 1980 y 1990, el precio medio nacional de la vivienda osciló entre 2,9 y 3,1 veces el ingreso familiar medio. En cambio, esta relación aumentó a 4,0 en 2004 y a 4,6 en 2006. [304] Esta burbuja inmobiliaria hizo que muchos propietarios refinanciaran sus viviendas a tipos de interés más bajos o financiaran el gasto de consumo contratando segundas hipotecas garantizadas por la apreciación de los precios.

En un programa ganador del premio Peabody , los corresponsales de la NPR argumentaron que una "gigante masa de dinero" (representada por 70 billones de dólares en inversiones de renta fija en todo el mundo) buscaba rendimientos más altos que los ofrecidos por los bonos del Tesoro de Estados Unidos a principios de la década. Esta masa de dinero había duplicado su tamaño entre 2000 y 2007, pero la oferta de inversiones relativamente seguras y generadoras de ingresos no había crecido tan rápido. Los bancos de inversión de Wall Street respondieron a esta demanda con productos como los títulos respaldados por hipotecas y las obligaciones de deuda colateralizadas , a los que las agencias de calificación crediticia les asignaron calificaciones seguras . [3]

En efecto, Wall Street conectó este fondo de dinero al mercado hipotecario de Estados Unidos, con enormes comisiones que se acumulaban a lo largo de la cadena de suministro de hipotecas , desde el corredor hipotecario que vendía los préstamos hasta los pequeños bancos que financiaban a los corredores y los grandes bancos de inversión que estaban detrás de ellos. Hacia 2003, la oferta de hipotecas originadas en los estándares de préstamo tradicionales se había agotado, y la fuerte demanda continua comenzó a hacer bajar los estándares de préstamo. [3]

En particular, la obligación de deuda colateralizada permitió a las instituciones financieras obtener fondos de inversores para financiar préstamos de alto riesgo y de otro tipo, lo que prolongó o aumentó la burbuja inmobiliaria y generó grandes comisiones. Esto, en esencia, coloca los pagos en efectivo de múltiples hipotecas u otras obligaciones de deuda en un solo fondo del que se extraen valores específicos en una secuencia específica de prioridad. Los primeros en la fila recibieron calificaciones de grado de inversión de las agencias de calificación. Los valores con menor prioridad tenían calificaciones crediticias más bajas, pero teóricamente una tasa de retorno más alta sobre la cantidad invertida. [305]

En septiembre de 2008, los precios promedio de las viviendas en Estados Unidos habían disminuido más de un 20% desde su pico de mediados de 2006. [306] [307] A medida que los precios bajaban, los prestatarios con hipotecas de tasa ajustable no podían refinanciarlas para evitar los pagos más altos asociados con las tasas de interés en aumento y comenzaron a incurrir en impagos. Durante 2007, los prestamistas iniciaron procedimientos de ejecución hipotecaria sobre casi 1,3 millones de propiedades, un aumento del 79% con respecto a 2006. [308] Esta cifra aumentó a 2,3 millones en 2008, un aumento del 81% con respecto a 2007. [309] En agosto de 2008, aproximadamente el 9% de todas las hipotecas pendientes en Estados Unidos estaban en mora o en ejecución hipotecaria. [310] En septiembre de 2009, esta cifra había aumentado al 14,4%. [311] [312]

Después de que estallara la burbuja, el economista australiano John Quiggin escribió: "Y, a diferencia de la Gran Depresión, esta crisis fue enteramente producto de los mercados financieros. No hubo nada parecido a la agitación de posguerra de los años 1920, las luchas por la convertibilidad del oro y las reparaciones, o el arancel Smoot-Hawley , todos los cuales han compartido la culpa por la Gran Depresión". En cambio, Quiggin atribuye la culpa por el colapso casi total de 2008 a los mercados financieros, a las decisiones políticas de regularlos a la ligera y a las agencias de calificación que tenían incentivos egoístas para otorgar buenas calificaciones. [313]

Condiciones de crédito fáciles

Los tipos de interés más bajos estimularon el endeudamiento. Entre 2000 y 2003, la Reserva Federal redujo el tipo de interés de los fondos federales del 6,5% al 1,0%. [314] [315] Esto se hizo para suavizar los efectos del colapso de la burbuja puntocom y los ataques del 11 de septiembre , así como para combatir un riesgo percibido de deflación . [316] Ya en 2002, era evidente que el crédito estaba impulsando la vivienda en lugar de la inversión empresarial, ya que algunos economistas llegaron al extremo de defender que la Reserva Federal "necesita crear una burbuja inmobiliaria para reemplazar la burbuja del Nasdaq". [317] Además, estudios empíricos que utilizan datos de países avanzados muestran que el crecimiento excesivo del crédito contribuyó en gran medida a la gravedad de la crisis. [ 318 ]

Bernanke explicó que entre 1996 y 2004, el déficit de cuenta corriente de Estados Unidos aumentó en 650.000 millones de dólares, pasando del 1,5% al 5,8% del PIB. Para financiar estos déficits, el país tuvo que pedir prestado grandes sumas de dinero al exterior, gran parte de ellas a países con superávits comerciales, principalmente las economías emergentes de Asia y los países exportadores de petróleo. La identidad de la balanza de pagos exige que un país (como Estados Unidos) que tenga un déficit de cuenta corriente tenga también un superávit de cuenta de capital (inversión) de la misma cuantía. Por consiguiente, grandes y crecientes cantidades de fondos extranjeros (capital) fluyeron hacia Estados Unidos para financiar sus importaciones.

Todo esto creó una demanda de diversos tipos de activos financieros, lo que elevó los precios de esos activos y redujo las tasas de interés. Los inversores extranjeros tenían esos fondos para prestar porque tenían tasas de ahorro personales muy altas (hasta el 40% en China) o porque los precios del petróleo eran altos. Ben Bernanke se refirió a esto como un " exceso de ahorro ". [320]

A flood of funds (capital or liquidity) reached the U.S. financial markets. Foreign governments supplied funds by purchasing Treasury bonds and thus avoided much of the direct effect of the crisis. U.S. households, used funds borrowed from foreigners to finance consumption or to bid up the prices of housing and financial assets. Financial institutions invested foreign funds in mortgage-backed securities.[citation needed]

The Fed then raised the Fed funds rate significantly between July 2004 and July 2006.[321] This contributed to an increase in one-year and five-year adjustable-rate mortgage (ARM) rates, making ARM interest rate resets more expensive for homeowners.[322] This may have also contributed to the deflating of the housing bubble, as asset prices generally move inversely to interest rates, and it became riskier to speculate in housing.[323][324] U.S. housing and financial assets dramatically declined in value after the housing bubble burst.[325][44]

Weak and fraudulent underwriting practices

Subprime lending standards declined in the U.S.: in early 2000, a subprime borrower had a FICO score of 660 or less. By 2005, many lenders dropped the required FICO score to 620, making it much easier to qualify for prime loans and making subprime lending a riskier business. Proof of income and assets were de-emphasized. Loans at first required full documentation, then low documentation, then no documentation. One subprime mortgage product that gained wide acceptance was the no income, no job, no asset verification required (NINJA) mortgage. Informally, these loans were aptly referred to as "liar loans" because they encouraged borrowers to be less than honest in the loan application process.[326] Testimony given to the Financial Crisis Inquiry Commission by whistleblowerRichard M. Bowen III, on events during his tenure as the Business Chief Underwriter for Correspondent Lending in the Consumer Lending Group for Citigroup, where he was responsible for over 220 professional underwriters, suggests that by 2006 and 2007, the collapse of mortgage underwriting standards was endemic. His testimony stated that by 2006, 60% of mortgages purchased by Citigroup from some 1,600 mortgage companies were "defective" (were not underwritten to policy, or did not contain all policy-required documents)—this, despite the fact that each of these 1,600 originators was contractually responsible (certified via representations and warrantees) that its mortgage originations met Citigroup standards. Moreover, during 2007, "defective mortgages (from mortgage originators contractually bound to perform underwriting to Citi's standards) increased ... to over 80% of production".[327]

In separate testimony to the Financial Crisis Inquiry Commission, officers of Clayton Holdings, the largest residential loan due diligence and securitization surveillance company in the United States and Europe, testified that Clayton's review of over 900,000 mortgages issued from January 2006 to June 2007 revealed that scarcely 54% of the loans met their originators' underwriting standards. The analysis (conducted on behalf of 23 investment and commercial banks, including 7 "too big to fail" banks) additionally showed that 28% of the sampled loans did not meet the minimal standards of any issuer. Clayton's analysis further showed that 39% of these loans (i.e. those not meeting any issuer's minimal underwriting standards) were subsequently securitized and sold to investors.[328][329]

Predatory lending

Predatory lending refers to the practice of unscrupulous lenders, enticing borrowers to enter into "unsafe" or "unsound" secured loans for inappropriate purposes.[330][331][332]

In June 2008, Countrywide Financial was sued by then California Attorney GeneralJerry Brown for "unfair business practices" and "false advertising", alleging that Countrywide used "deceptive tactics to push homeowners into complicated, risky, and expensive loans so that the company could sell as many loans as possible to third-party investors".[333] In May 2009, Bank of America modified 64,000 Countrywide loans as a result.[334] When housing prices decreased, homeowners in ARMs then had little incentive to pay their monthly payments, since their home equity had disappeared. This caused Countrywide's financial condition to deteriorate, ultimately resulting in a decision by the Office of Thrift Supervision to seize the lender. One Countrywide employee—who would later plead guilty to two counts of wire fraud and spent 18 months in prison—stated that, "If you had a pulse, we gave you a loan."[335]

Former employees from Ameriquest, which was United States' leading wholesale lender, described a system in which they were pushed to falsify mortgage documents and then sell the mortgages to Wall Street banks eager to make fast profits. There is growing evidence that such mortgage frauds may be a cause of the crisis.[336]

Deregulation and lack of regulation

According to Barry Eichengreen, the roots of the financial crisis lay in the deregulation of financial markets.[337] A 2012 OECD study[338] suggest that bank regulation based on the Basel accords encourage unconventional business practices and contributed to or even reinforced the financial crisis. In other cases, laws were changed or enforcement weakened in parts of the financial system. Key examples include:

In November 1999, U.S. President Bill Clinton signed into law the Gramm–Leach–Bliley Act, which repealed provisions of the Glass-Steagall Act that prohibited a bank holding company from owning other financial companies. The repeal effectively removed the separation that previously existed between Wall Street investment banks and depository banks, providing a government stamp of approval for a universal risk-taking banking model. Investment banks such as Lehman became competitors with commercial banks.[342] Some analysts say that this repeal directly contributed to the severity of the crisis, while others downplay its impact since the institutions that were greatly affected did not fall under the jurisdiction of the act itself.[343][344]

In 2004, the U.S. Securities and Exchange Commission relaxed the net capital rule, which enabled investment banks to substantially increase the level of debt they were taking on, fueling the growth in mortgage-backed securities supporting subprime mortgages. The SEC conceded that self-regulation of investment banks contributed to the crisis.[345][346]

Financial institutions in the shadow banking system are not subject to the same regulation as depository banks, allowing them to assume additional debt obligations relative to their financial cushion or capital base.[347] This was the case despite the Long-Term Capital Management debacle in 1998, in which a highly leveraged shadow institution failed with systemic implications and was bailed out.

Regulators and accounting standard-setters allowed depository banks such as Citigroup to move significant amounts of assets and liabilities off-balance sheet into complex legal entities called structured investment vehicles, masking the weakness of the capital base of the firm or degree of leverage or risk taken. Bloomberg News estimated that the top four U.S. banks will have to return between $500 billion and $1 trillion to their balance sheets during 2009.[348] This increased uncertainty during the crisis regarding the financial position of the major banks.[349] Off-balance sheet entities were also used in the Enron scandal, which brought down Enron in 2001.[350]

As early as 1997, Federal Reserve chairman Alan Greenspan fought to keep the derivatives market unregulated.[351] With the advice of the Working Group on Financial Markets,[352] the U.S. Congress and President Bill Clinton allowed the self-regulation of the over-the-counter derivatives market when they enacted the Commodity Futures Modernization Act of 2000. Written by Congress with lobbying from the financial industry, it banned the further regulation of the derivatives market. Derivatives such as credit default swaps (CDS) can be used to hedge or speculate against particular credit risks without necessarily owning the underlying debt instruments. The volume of CDS outstanding increased 100-fold from 1998 to 2008, with estimates of the debt covered by CDS contracts, as of November 2008, ranging from US$33 to $47 trillion. Total over-the-counter (OTC) derivative notional value rose to $683 trillion by June 2008.[353]Warren Buffett famously referred to derivatives as "financial weapons of mass destruction" in early 2003.[354][355]

A 2011 paper suggested that Canada's avoidance of a banking crisis in 2008 (as well as in prior eras) could be attributed to Canada possessing a single, powerful, overarching regulator, while the United States had a weak, crisis prone and fragmented banking system with multiple competing regulatory bodies.[356]

Increased debt burden or overleveraging

Leverage ratios of investment banks increased significantly between 2003 and 2007Household debt relative to disposable income and GDP

Prior to the crisis, financial institutions became highly leveraged, increasing their appetite for risky investments and reducing their resilience in case of losses. Much of this leverage was achieved using complex financial instruments such as off-balance sheet securitization and derivatives, which made it difficult for creditors and regulators to monitor and try to reduce financial institution risk levels.[357][verification needed]

U.S. households and financial institutions became increasingly indebted or overleveraged during the years preceding the crisis.[358] This increased their vulnerability to the collapse of the housing bubble and worsened the ensuing economic downturn.[359] Key statistics include:

Free cash used by consumers from home equity extraction doubled from $627 billion in 2001 to $1,428 billion in 2005 as the housing bubble built, a total of nearly $5 trillion over the period, contributing to economic growth worldwide.[31][32][33] U.S. home mortgage debt relative to GDP increased from an average of 46% during the 1990s to 73% during 2008, reaching $10.5 trillion (c. $14.6 trillion in 2023[294]).[30]

U.S. household debt as a percentage of annual disposable personal income was 127% at the end of 2007, versus 77% in 1990.[358] In 1981, U.S. private debt was 123% of GDP; by the third quarter of 2008, it was 290%.[360]

From 2004 to 2007, the top five U.S. investment banks each significantly increased their financial leverage, which increased their vulnerability to a financial shock. Changes in capital requirements, intended to keep U.S. banks competitive with their European counterparts, allowed lower risk weightings for AAA-rated securities. The shift from first-loss tranches to AAA-rated tranches was seen by regulators as a risk reduction that compensated the higher leverage.[361] These five institutions reported over $4.1 trillion in debt for fiscal year 2007, about 30% of U.S. nominal GDP for 2007. Lehman Brotherswent bankrupt and was liquidated, Bear Stearns and Merrill Lynch were sold at fire-sale prices, and Goldman Sachs and Morgan Stanley became commercial banks, subjecting themselves to more stringent regulation. With the exception of Lehman, these companies required or received government support.[362]

Fannie Mae and Freddie Mac, two U.S. government-sponsored enterprises, owned or guaranteed nearly $5 trillion (c. $6.95 trillion in 2023[294]) trillion in mortgage obligations at the time they were placed into conservatorship by the U.S. government in September 2008.[363][364]

These seven entities were highly leveraged and had $9 trillion in debt or guarantee obligations; yet they were not subject to the same regulation as depository banks.[347][365]

Behavior that may be optimal for an individual, such as saving more during adverse economic conditions, can be detrimental if too many individuals pursue the same behavior, as ultimately one person's consumption is another person's income. Too many consumers attempting to save or pay down debt simultaneously is called the paradox of thrift and can cause or deepen a recession. Economist Hyman Minsky also described a "paradox of deleveraging" as financial institutions that have too much leverage (debt relative to equity) cannot all de-leverage simultaneously without significant declines in the value of their assets.[359]

Once this massive credit crunch hit, it didn't take long before we were in a recession. The recession, in turn, deepened the credit crunch as demand and employment fell, and credit losses of financial institutions surged. Indeed, we have been in the grips of precisely this adverse feedback loop for more than a year. A process of balance sheet deleveraging has spread to nearly every corner of the economy. Consumers are pulling back on purchases, especially on durable goods, to build their savings. Businesses are cancelling planned investments and laying off workers to preserve cash. And financial institutions are shrinking assets to bolster capital and improve their chances of weathering the current storm. Once again, Minsky understood this dynamic. He spoke of the paradox of deleveraging, in which precautions that may be smart for individuals and firms—and indeed essential to return the economy to a normal state—nevertheless magnify the distress of the economy as a whole.[359]

Financial innovation and complexity

IMF Diagram of CDO and RMBS

The term financial innovation refers to the ongoing development of financial products designed to achieve particular client objectives, such as offsetting a particular risk exposure (such as the default of a borrower) or to assist with obtaining financing. Examples pertinent to this crisis included: the adjustable-rate mortgage; the bundling of subprime mortgages into mortgage-backed securities (MBS) or collateralized debt obligations (CDO) for sale to investors, a type of securitization; and a form of credit insurance called credit default swaps (CDS). The usage of these products expanded dramatically in the years leading up to the crisis. These products vary in complexity and the ease with which they can be valued on the books of financial institutions.[citation needed]

CDO issuance grew from an estimated $20 billion in Q1 2004 to its peak of over $180 billion by Q1 2007, then declined back under $20 billion by Q1 2008. Further, the credit quality of CDO's declined from 2000 to 2007, as the level of subprime and other non-prime mortgage debt increased from 5% to 36% of CDO assets. As described in the section on subprime lending, the CDS and portfolio of CDS called synthetic CDO enabled a theoretically infinite amount to be wagered on the finite value of housing loans outstanding, provided that buyers and sellers of the derivatives could be found. For example, buying a CDS to insure a CDO ended up giving the seller the same risk as if they owned the CDO, when those CDO's became worthless.[366]

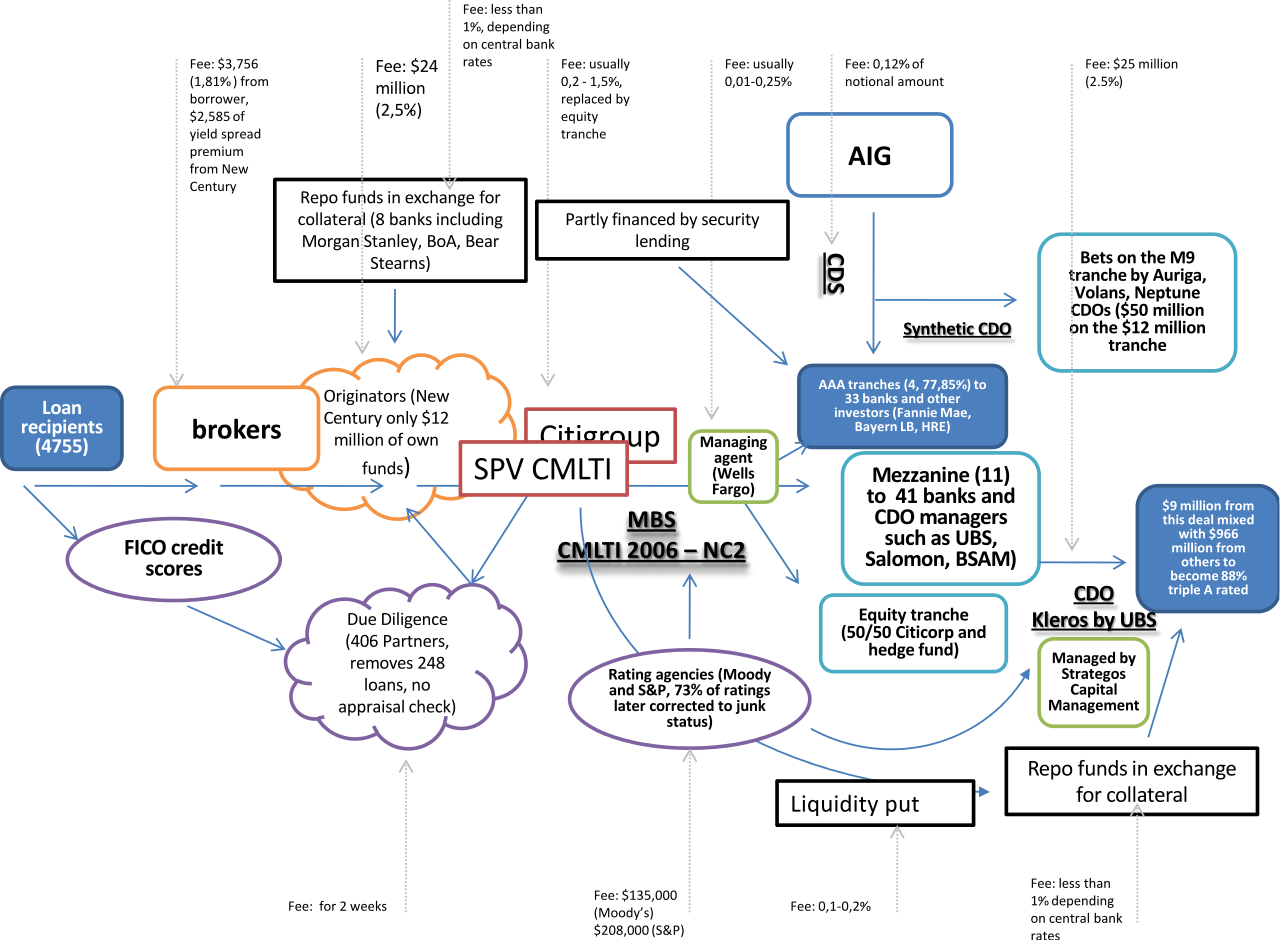

Diagram of CMLTI 2006 – NC2

This boom in innovative financial products went hand in hand with more complexity. It multiplied the number of actors connected to a single mortgage (including mortgage brokers, specialized originators, the securitizers and their due diligence firms, managing agents and trading desks, and finally investors, insurances and providers of repo funding). With increasing distance from the underlying asset these actors relied more and more on indirect information (including FICO scores on creditworthiness, appraisals and due diligence checks by third party organizations, and most importantly the computer models of rating agencies and risk management desks). Instead of spreading risk this provided the ground for fraudulent acts, misjudgments and finally market collapse.[367] Economists have studied the crisis as an instance of cascades in financial networks, where institutions' instability destabilized other institutions and led to knock-on effects.[368][369]

Martin Wolf, chief economics commentator at the Financial Times, wrote in June 2009 that certain financial innovations enabled firms to circumvent regulations, such as off-balance sheet financing that affects the leverage or capital cushion reported by major banks, stating: "an enormous part of what banks did in the early part of this decade—the off-balance-sheet vehicles, the derivatives and the 'shadow banking system' itself—was to find a way round regulation."[370]

Mortgage risks were underestimated by almost all institutions in the chain from originator to investor by underweighting the possibility of falling housing prices based on historical trends of the past 50 years. Limitations of default and prepayment models, the heart of pricing models, led to overvaluation of mortgage and asset-backed products and their derivatives by originators, securitizers, broker-dealers, rating-agencies, insurance underwriters and the vast majority of investors (with the exception of certain hedge funds).[371][372] While financial derivatives and structured products helped partition and shift risk between financial participants, it was the underestimation of falling housing prices and the resultant losses that led to aggregate risk.[372]